As the pandemic kept people at home, we saw a dramatic rise in at-home consumption of spirits and a shift in preferences towards more premium products. We believe both trends driven by the pandemic are sustainable trends.

Diageo is currently one of the 14 stocks in the Claremont Global portfolio. In this article we discuss how Diageo’s leading market position and unique portfolio of brands ― combined with strong category drivers ― has set the company up for long term success.

Diageo (DGE: LSE)

Diageo is the world’s largest producer of international spirits with a portfolio of over 200 brands sold in more than 180 countries. The company owns a nearly a quarter of the top 100 western-style spirits with key brands including Johnnie Walker, Smirnoff, Capitan Morgan, Baileys, Don Julio and Guinness. Diageo is also the only western company with exposure to Baijiu, the world’s largest spirit category, with a majority stake in Shui Jing Fang in China.

Diageo – key brands

Source: Company website

Superior execution shines in a crisis

The pandemic saw hospitality businesses (or on-trade) close across the world, which represents around one third of Diageo’s overall business. However, Diageo’s management was quick to adapt to changes in demand, occasions and channels. They activated in-store marketing, focused innovation towards convenience and invested in their online capability.

These series of actions paid off, driving a rapid recovery in sales and saw Diageo hold or grow off-trade share in over 85% of net sales in measured markets in FY21.

A portfolio that can stay ahead of the curve

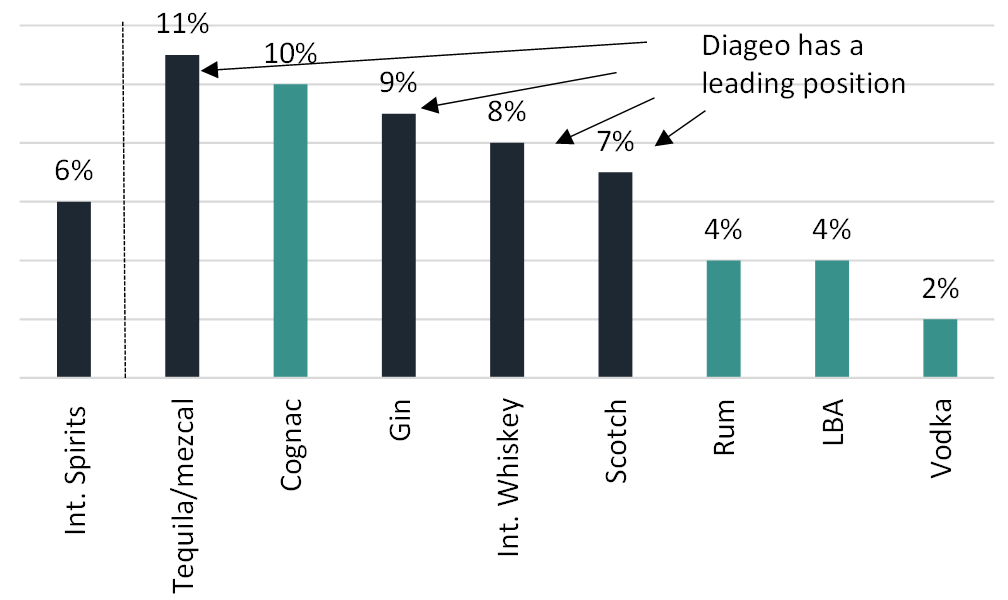

The key to Diageo’s success is having a well-diversified portfolio that can meet changes in consumer tastes. However, the company has also been able to acquire and build brands to shape their offer towards higher growth opportunities. Diageo’s portfolio is strongly placed as they hold a leading position in four out of the five fastest growing spirits categories (see chart below). Diageo is number one in Scotch (1.7x the scale of the nearest competitor), Gin (2x the scale of the nearest peer) and Canadian Whiskey and top five in Tequila (fastest-growing portfolio).

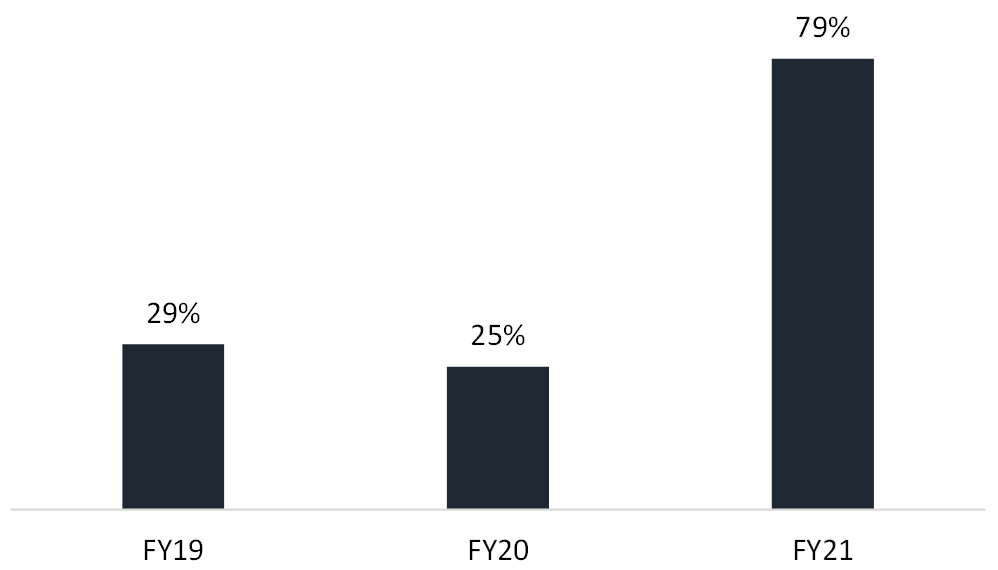

Diageo’s success in Tequila (see chart below) is a good example of their ability to identify early stage shifts in consumer preferences. Diageo acquired the remainder of their stake in Don Julio in 2014 and acquired Casamigos in 2017. Since acquiring Don Julio, they have increased sales seven-fold and Casamigos eleven-fold. Don Julio 1942 (the aged version) is now the single-biggest luxury spirit brands in the US.

Diageo anticipates that 50 per cent of their incremental growth from FY23-26 will be driven by Tequila, which will make the agave spirit their second largest behind Scotch by FY26.

Global growth of retail sales value (RSV) by category 2020-25 compound annual growth rate (CAGR)

Source: Diageo CMD presentation Nov 2021, IWSR estimates

Diageo – Tequila organic sales growth

Source: Claremont Global, company data. Past performance is not a reliable indicator of future performance.

Penetration – spirits continue to be the winning category

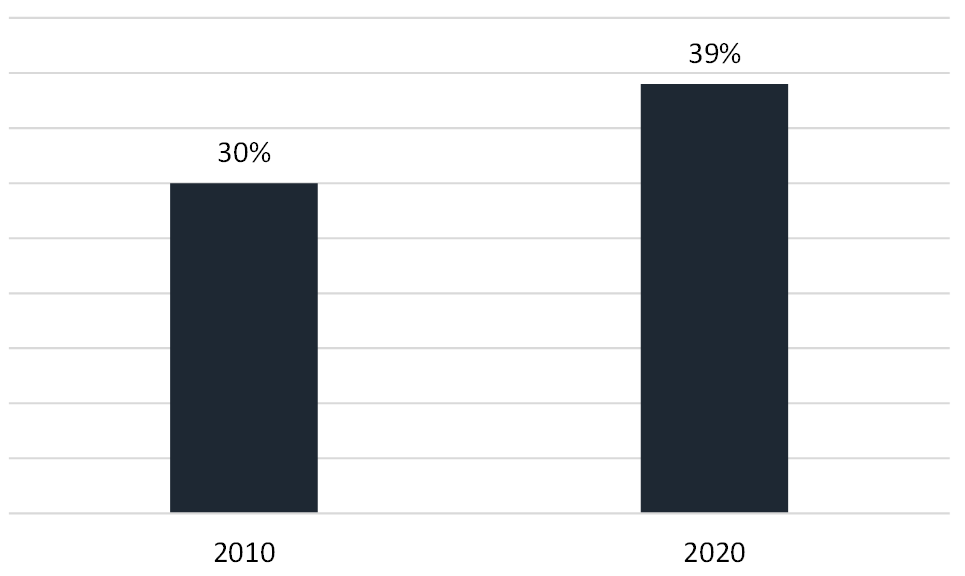

The spirits category has been winning market share from beer and wine over the last decade and now accounts for 39 per cent of the total global alcoholic beverage market (Total Beverage Alcohol or TBA), which is up from 30 per cent in 2010.

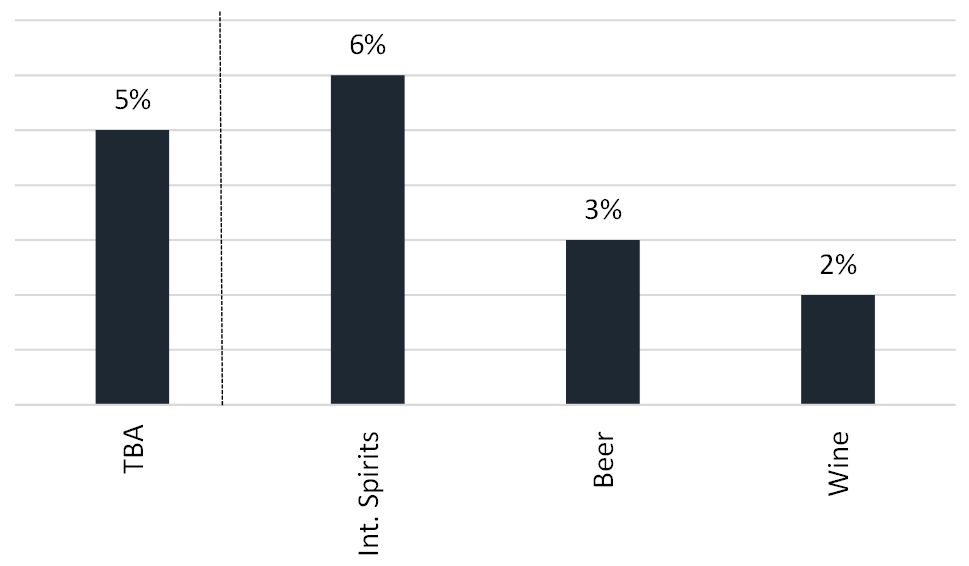

While this has accelerated during the pandemic, industry sources expect the consumer shift towards spirits to continue growing at 6 per cent per annum over 2020-25, which is around 3x faster than wine and around 2x faster than beer (source: Diageo, IWSR).

Each year more than 50 million consumers reach drinking age which supports growth and Diageo additionally recruits over 40 million new consumers each year.

Diageo is the largest international spirits producer, 1.5x the size of its nearest competitor and is well placed to benefit from the attractive category growth. However, there is plenty of room to grow as Diageo has only 4 per cent share of TBA and the company recently set the ambitious target to increase their TBA share by 50 per cent by 2030.

Spirits share of TBA

Source: Diageo CMD presentation Nov 2021, IWSR estimates.

Global growth of RSV by category (2020-25 CAGR)

Source: Diageo CMD presentation Nov 2021, IWSR estimates.

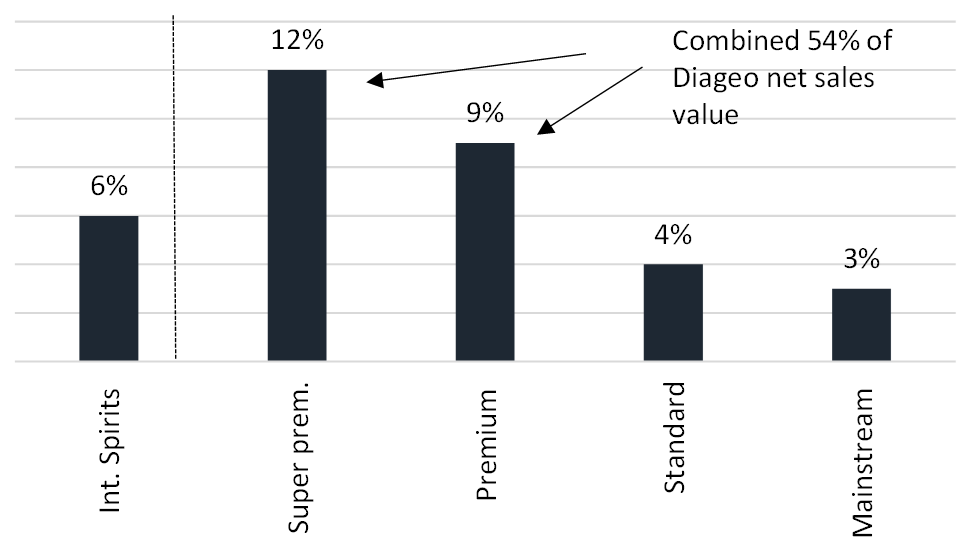

Premiumisation – looking higher and higher up the shelf

Premiumisation has been a key growth driver for Diageo as people are drinking less but opting for better quality alcohol ― whether it is moving from illicit alcohol to branded or from black to blue label. Across the industry super premium and premium price tiers have grown by 13 per cent and 9 per cent respectively over the last 10 years, well above budget friendly alternatives (source: Diageo/IWSR).

While this trend has also been boosted by lockdowns, at home consumption has remained resilient as hospitality venues reopen and we also expect consumers to drink higher quality beverages while they are out. This plays into Diageo’s key strength, as it generates over half of its business from the faster growing premium and super premium price tiers (see chart below).

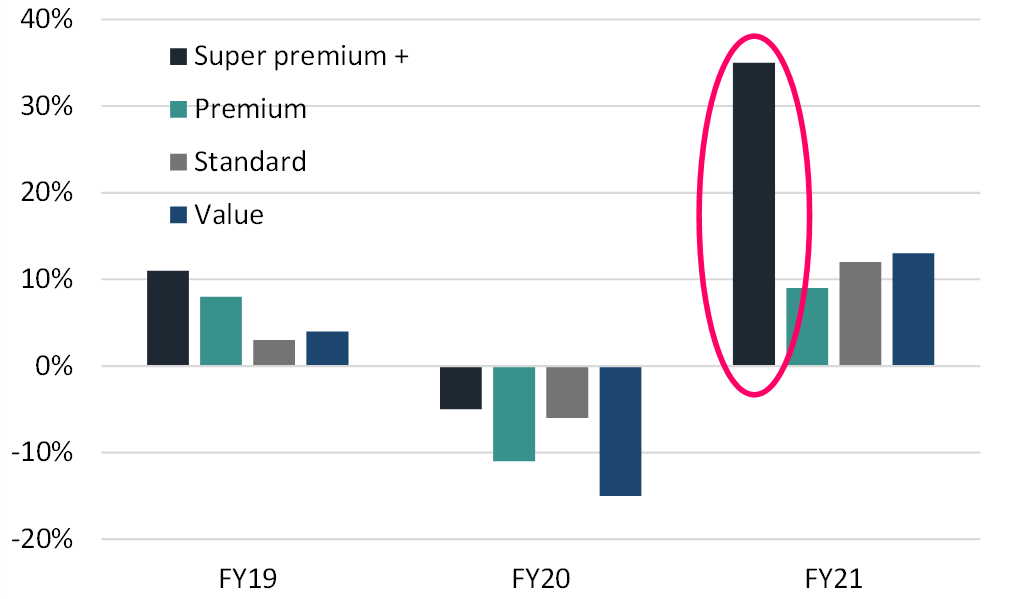

Diageo’s super premium+ price tier grew 35 per cent in FY21 (see chart below). We believe the acceleration in premiumisation is sustainable as household balance sheets remain robust and consumers continue to look for affordable luxuries. In the US, the average household spends only $17 per month on spirits, which offers plenty of room for upside.

Global growth of RSV by price tier (2020-25 CAGR)

Source: Diageo CMD presentation Nov 2021, IWSR estimates.

Diageo total value growth by price tier

Source: Claremont Global, company data. Past performance is not a reliable indicator of future performance

Why Diageo continues to be a global leader

We are attracted to Diageo’s global leading position and diversification across regions and spirits.

We see Diageo as a quasi-staple, offering solid top line organic growth of 5-7 per cent (a target they recently upgraded), with an attractive and expanding operating margin of close to 30 per cent. The company has also delivered 20 years of dividend increases.

Diageo’s performance through the pandemic provided clear evidence in the strength of the management team and benefits from reinvestment in recent years, that has made Diageo a more agile company. Diageo is also an industry leader in environmental, social and governance (ESG) and as part of their 2030 goals have made sizeable commitments around positive drinking, inclusion and diversity and sustainability (including net zero carbon emissions across direct operations).